August air cargo growth remains strong

Share

Share

The International Air Transport Association (IATA) released August 2021 data for global air cargo markets showing that demand continued its strong growth trend but pressure on capacity is rising.

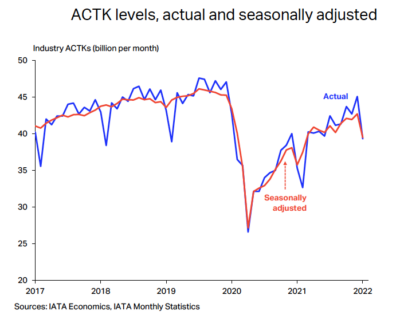

Global demand, measured in cargo tonne-kilometers (CTKs), was up 7.7 percent compared to August 2019 (8.6 percent for international operations). Overall growth remains strong compared to the long-term average growth trend of around 4.7 percent.

The pace of growth slowed slightly compared to July, which saw demand increase 8.8 percent (against pre-COVID-19 levels).

Cargo capacity recovery paused in August, down 12.2 percent compared to August 2019 (13.2 percent for international operations). In month-on-month terms, capacity fell by 1.6 percent – the largest drop since January 2021.

Economic conditions continue to support air cargo growth but are slightly weaker than in the previous months indicating that global manufacturing growth has peaked:

“Air cargo demand had another strong month in August, up 7.7 percent compared to pre-COVID levels. Many of the economic indicators point to a strong year-end peak season. With international travel still severely depressed, there are fewer passenger planes offering belly capacity for cargo. And supply chain bottlenecks could intensify as businesses continue to ramp up production,” said Willie Walsh, IATA’s Director General.

|

1 % of industry CTKs in 2020 2 Change in load factor vs 2019 3 Load factor level

Asia-Pacific airlines saw their international air cargo volumes increase 3.0 percent in August 2021 compared to the same month in 2019.This was a slowdown in demand compared to the previous month’s 4.4 percent expansion. Demand is being affected by an easing in growth momentum in key activity indicators in Asia, and by congested supply chains especially on Within Asia and Europe-Asia routes. International capacity is significantly constrained in the region, down 21.7 percent vs. August 2019.

North American carriers posted an 18 percent increase in international cargo volumes in August 2021 compared to August 2019. New export orders and demand for faster shipping times are underpinning the North American performance. The downside risk from capacity constraints is high; international cargo capacity remains restricted and many of the key air cargo hubs are reporting severe congestion, including Los Angeles and Chicago. International capacity decreased 6.6 percent.

European carriers saw a six percent increase in international cargo volumes in August 2021 compared to the same month in 2019. This was on a par with July’s performance. Manufacturing activity, orders and long supplier delivery times remain favorable to air cargo demand. International capacity decreased 13.6 percent.

Middle Eastern carriers experienced an 15.4 percent rise in international cargo volumes in August 2021 versus August 2019, an improvement compared to the previous month (13.4 percent). The large Middle East–Asia trade lanes continue to post strong performance. International capacity decreased 5.1 percent.

Latin American carriers reported a decline of 14 percent in international cargo volumes in August compared to the 2019 period, which was the weakest performance of all regions. Capacity remains significantly constrained in the region, with international capacity decreasing 27.1 percent in August, the largest fall of any region.

African airlines’ saw international cargo volumes increase by 33.9 percent in August, the largest increase of all regions. Investment flows along the Africa-Asia route continue to drive the regional outcomes with volumes on the route up 26.4 percent over two years ago. International capacity decreased 2.1 percent.

Leave a Reply